June 30, 2026

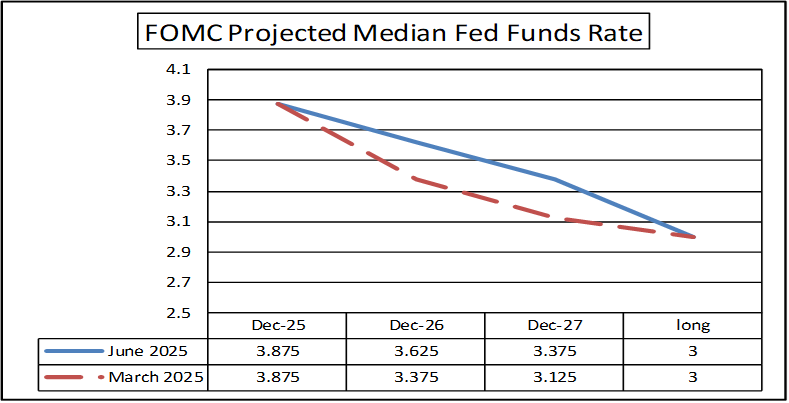

The June 16-17 Federal Open Market Committee (FOMC) meeting, the first with Kevin Warsh as Chairman, was termed as a “hawkish hold” as the policy statement dropped the easing bias. Holding policy rates steady and the removal of the easing bias were widely expected. It was considered hawkish as half of the Committee members providing rate projections in the “dot plot” penciled in higher policy rates by year end. The Fed had little choice but to hold the targeted fed funds range unchanged at 3.5% to 3.75% at this meeting with the labor market appearing to have steadied and the central bank’s reluctance to adjust policy rates in response to temporary energy shocks. The combination of these factors has provided the Fed with plenty of flexibility to be patient.

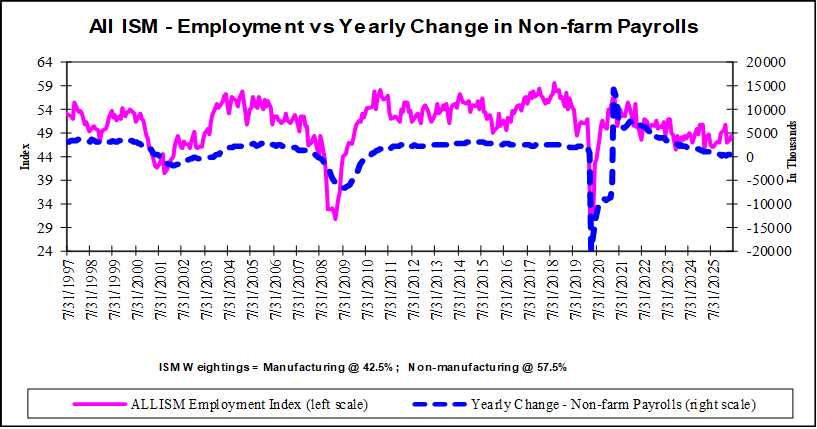

The April job openings and May employment reports gave the Fed some welcome assurance to remain on hold with broad-based gains across industries. These reports are backward looking, however, while some leading labor market indicators may be seeing dark clouds on the horizon. Initial jobless claims, while still historically low, have started trending upward, a survey of small businesses is pointing to slower job creation ahead and the manufacturing and service sectors surveys by the Institute for Supply Management (ISM) have the employment component in negative territory. Spillover effects from the war may still hit the labor market with a lag. If the consumer slows it could weigh on hiring. Consumer spending, while resilient to date, could become tenuous with a rapidly falling savings rate and weak consumer confidence that eventually may lead to a downward shift in demand.

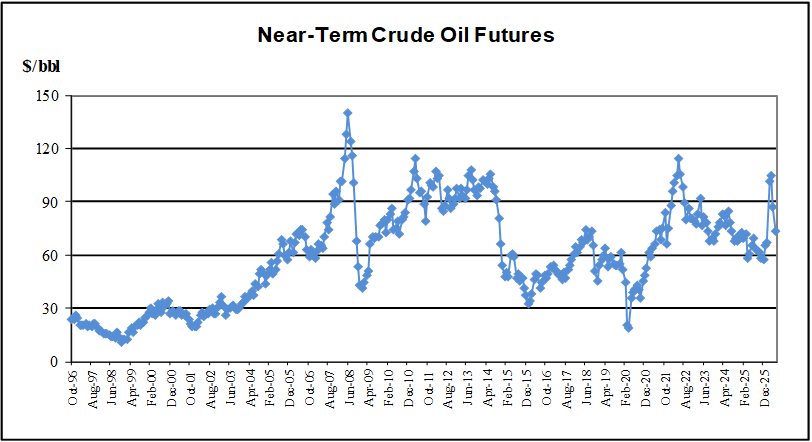

Inflation remains sticky. May’s headline CPI and PPI hit their highest level in three years. Year-over-year rates rose to 4.2% for CPI and 6.5% for PPI. May’s PCE Deflators, reportedly the Fed’s preferred inflation gauge, posted year-over-year rates of 4.1% for the headline and 3.4% for core. The markets, however, reacted to some positives in the reports. One, the absence of significant energy-price passthrough into the core (excluding food & energy) measures. Two, some economists even ventured to say that the May’s reports may be the peak in headline gauges as the price of oil declined sharply in June as Iran and the US agreed to a truce re-opening the Strait of Hormuz. Gasoline prices have started to follow oil prices lower.

In his first post-FOMC meeting press conference, Fed Chairman Kevin Warsh struck a more hawkish tone than expected. He said the FOMC was “unambiguously and unanimously” resolved to fight inflation. This had the markets fully pricing in at least one rate hike by the end of the year. But, there are arguments for the Fed to remain patient and be on hold for longer than expected. One argument is for the Fed to await developments in the Middle East war. The Committee may also want to await results from the five task forces created by Warsh and composed of internal and external experts. The task forces are charge with assessing communications, the balance sheet, data sourcing, the inflation framework and Artificial Intelligence (AI) implications for productivity and employment.

Full Fusion

Full Fusion