May 31, 2026

Based on comments by some Fed officials, the Central Bank may be shifting their focus to the inflation side of their dual mandate. Labor-market conditions seem to have stabilized but remain fragile. On the other hand, inflation has run above the Fed’s target for six years now and is moving in the wrong direction. The March Job Openings and Labor Turnover Survey (JOLTS) showed that while job openings decreased slightly, there was a pickup in hiring. The ADP Private Employment Report surprised to the upside for the second consecutive month, as did non-farm payrolls in the employment report. Initial and continuing claims for unemployment benefits remain low by historical standards and the unemployment rate in April held steady at 4.3%.

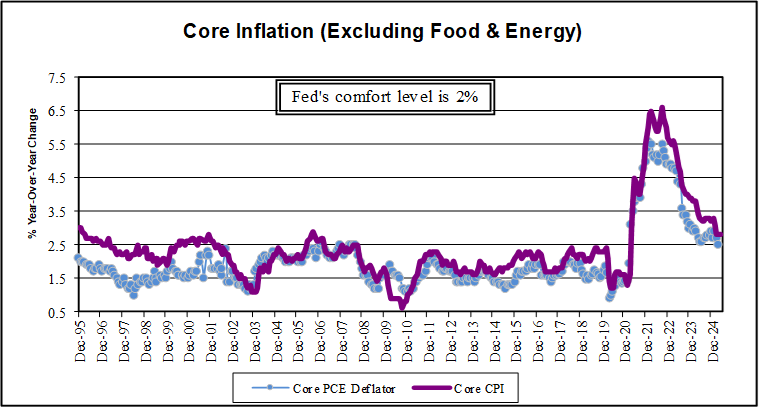

Inflation data, however, will likely get worse before it gets better. The energy prices have passed through the Consumer Price Index (CPI), directly and indirectly. The April report revealed another month of strong price increases. On a twelve month basis, CPI jumped to 3.8%, the fastest rate of growth in three years. Core (excluding food & energy) moved up to 2.8% year-over-year from 2.6% in March. Economists believe that energy-driven cost increases will eventually spill over to core CPI, but the impact will be tempered by ongoing housing disinflation, a lukewarm labor market and fading tariff effects. Even as the Fed typically prefers to look through often volatile categories, consumers’ inflation perceptions are heavily driven by them. Prices at the gas pump and the grocery store get their attention, to say nothing of mortgage rates, and the Fed needs to see inflation expectations remain well anchored. The Fed also can’t ignore their “preferred measure of inflation.” Personal Consumption Expenditures (PCE). The headline number matched the year-over-year CPI rate of 3.8%, while the core number was somewhat higher at 3.3%.

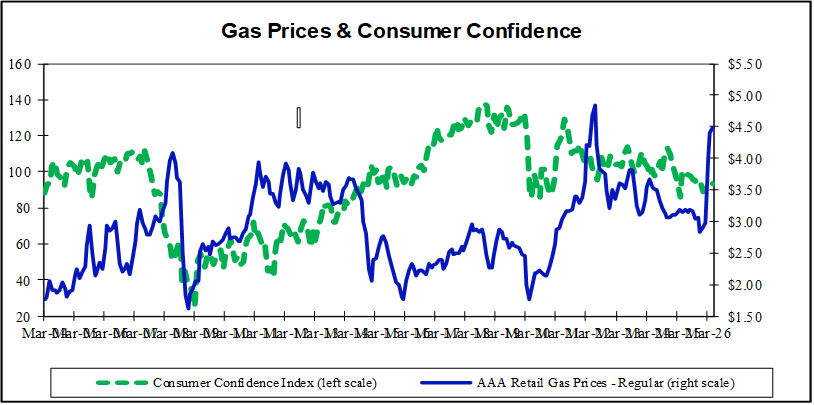

To date, the consumer has shown resilience, but it may be diminishing. U.S. retail sales advanced a third consecutive month, but shoppers pulled back on spending in April as higher fuel prices meant less money left over for some non-essentials. Sales rose 0.5% for the month, a slowdown from a 1.6% monthly change in March. The bottom line is that elevated prices of gas and food boosted April’s headline sales, but underlying consumer demand softened. With consumer sentiment measures at or near record lows, wage growth not keeping up with rising price pressures and the savings rate hitting a six-year low, a broader pullback in household spending is clearly a rising risk.

The path ahead for the Federal Reserve’s policy rates depend largely on how long the Middle East conflict disrupts supplies of oil and other goods. The Fed will focus on two questions. First, how much inflation will supply shortages produce and how long will that pressure persist? Second, how much destruction in demand will result from higher prices, and how damaging may that be to the labor market? As the answers become clearer, the Fed will choose which side of the dual mandate to address, full employment or stable prices.

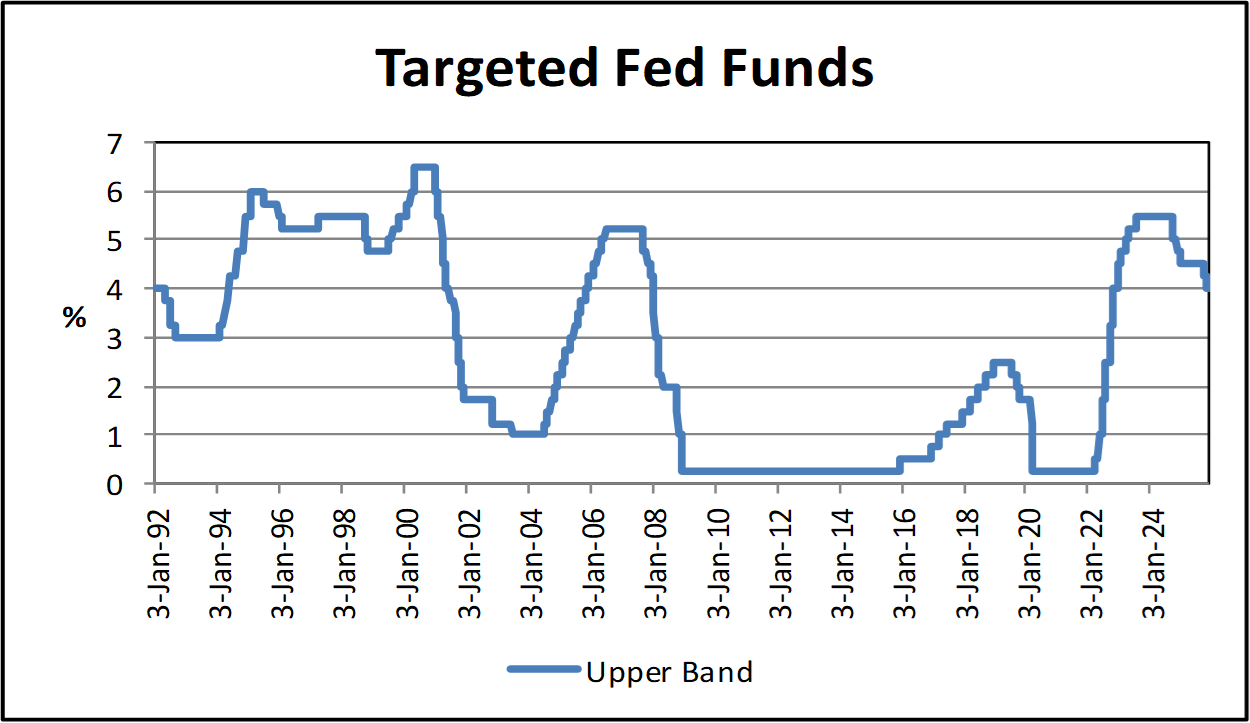

The Fed will announce its next interest rate decision June 17 with the new Fed Chairman Kevin Warsh at the helm. The central bank will likely have little choice but to hold the targeted fed funds range steady at 3.50% to 3.75% for the fourth consecutive meeting due to heightened uncertainty around the economic impacts of the war. The focus of the financial markets will likely center on what can be gleaned about future moves, whether the next move is more likely up than down. Until recently, the financial markets were anticipating two quarter point cuts in the fed funds rate this year, now they are building in the probability of a rate hike.

Kevin Warch comes to the Fed with an ambitious agenda. He has called for “regime change” in policy making, including changing the data the Fed makes its policy decisions on, removing forward guidance from its communications and shrinking the balance sheet. Until recently he was advocating lower rates, and that appeared as a key driver of his nomination by the President. He returns to the Fed as a highly respected economist and former Fed Governor but will need to work methodically if he is to become an effective leader of this group with eighteen other existing members. Only time will tell how long the war will last and what the long-term impact will be. Until more clarity emerges, the Fed will have a hard time moving in either direction. Financial markets will move, however, as they try to predict which side of the dual mandate ultimately gets the Fed back into action, and how effective Kevin Warsh will ultimately be in leading this group.

Full Fusion

Full Fusion