Our Investment Portfolio Reporting service provides record-keeping for all your investments, including structured notes, pass-through pools, and collateralized mortgage obligations (CMOs). You’ll have concise and accurate monthly accruals for interest, amortization, and accretion. A flexible general ledger interface option can be used to create entries for accruals, payments, and transactions.

How we make it easy…

Investment reporting doesn’t get easier than this! Once you’re up and running, you just send us a copy of your confirmations as you buy and sell investments in your portfolio. We update your investment portfolio and generate your reports. Each month you receive income accruals and appraisals on your investments. You also receive other important information to help you prudently manage your investments.

Each client is assigned an experienced customer service representative who assists in reconciling your portfolio to the general ledger and is available to answer your questions on the reports. FinSer’s service includes flexible cut-off dates and quick turnaround of the reports.

Key Features

- Monthly Reporting

- Entries for interest accruals and amortization/accretion

- Principal and interest payment verification reports

- Reports organized by investment type and ASC 320 (FASB 115) category

- General ledger reconciliation reports

- Portfolio Summary and Maturity Distribution reports

- Cash flow and budget projection reports

- Regulatory reporting for banks and credit unions

- Fair market values

- Quarterly Shock Test

- -400 to +500 basis point shock

- Summary reports show the effect of rate changes on an entire portfolio

- Reports by investment type and individual security

- Quarterly Interest Rate and Bond Market Recap (commentary)

- Year-to-Date Reports

- Quarterly recap of year-to-date purchases, sales, calls, and maturities

- Year-to-date amortization, accretion, and interest accrued

- Roll forward reporting (summary, investment type, and security)

- Contractual Maturity Schedule

- Unrealized Gain/Loss Summary

- Data Interfaces

- Data file with over 175 fields per cusip

- Optional General Ledger interface for accruals, payments, transactions

May 31, 2026

Based on comments by some Fed officials, the Central Bank may be shifting their focus to the inflation side of their dual mandate. Labor-market conditions seem to have stabilized but remain fragile. On the other hand, inflation has run above the Fed’s target for six years now and is moving in the wrong direction. The March Job Openings and Labor Turnover Survey (JOLTS) showed that while job openings decreased slightly, there was a pickup in hiring. The ADP Private Employment Report surprised to the upside for the second consecutive month, as did non-farm payrolls in the employment report. Initial and continuing claims for unemployment benefits remain low by historical standards and the unemployment rate in April held steady at 4.3%.

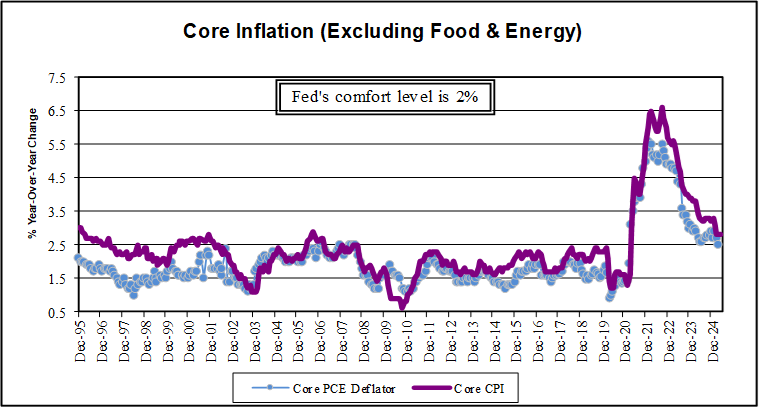

Inflation data, however, will likely get worse before it gets better. The energy prices have passed through the Consumer Price Index (CPI), directly and indirectly. The April report revealed another month of strong price increases. On a twelve month basis, CPI jumped to 3.8%, the fastest rate of growth in three years. Core (excluding food & energy) moved up to 2.8% year-over-year from 2.6% in March. Economists believe that energy-driven cost increases will eventually spill over to core CPI, but the impact will be tempered by ongoing housing disinflation, a lukewarm labor market and fading tariff effects. Even as the Fed typically prefers to look through often volatile categories, consumers’ inflation perceptions are heavily driven by them. Prices at the gas pump and the grocery store get their attention, to say nothing of mortgage rates, and the Fed needs to see inflation expectations remain well anchored. The Fed also can’t ignore their “preferred measure of inflation.” Personal Consumption Expenditures (PCE). The headline number matched the year-over-year CPI rate of 3.8%, while the core number was somewhat higher at 3.3%.

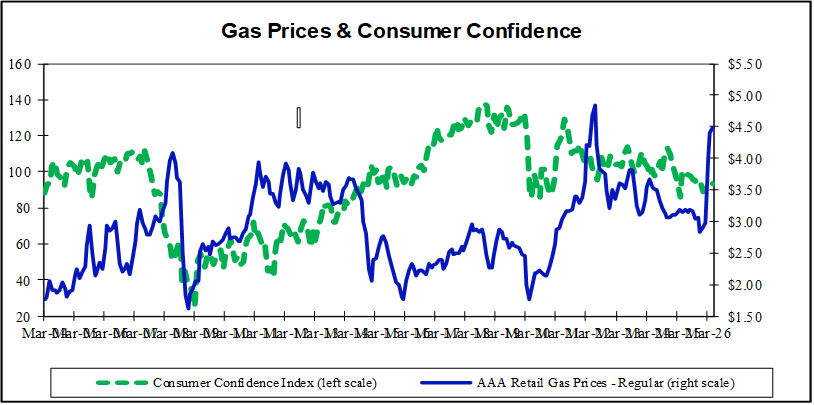

To date, the consumer has shown resilience, but it may be diminishing. U.S. retail sales advanced a third consecutive month, but shoppers pulled back on spending in April as higher fuel prices meant less money left over for some non-essentials. Sales rose 0.5% for the month, a slowdown from a 1.6% monthly change in March. The bottom line is that elevated prices of gas and food boosted April’s headline sales, but underlying consumer demand softened. With consumer sentiment measures at or near record lows, wage growth not keeping up with rising price pressures and the savings rate hitting a six-year low, a broader pullback in household spending is clearly a rising risk.

The path ahead for the Federal Reserve’s policy rates depend largely on how long the Middle East conflict disrupts supplies of oil and other goods. The Fed will focus on two questions. First, how much inflation will supply shortages produce and how long will that pressure persist? Second, how much destruction in demand will result from higher prices, and how damaging may that be to the labor market? As the answers become clearer, the Fed will choose which side of the dual mandate to address, full employment or stable prices.

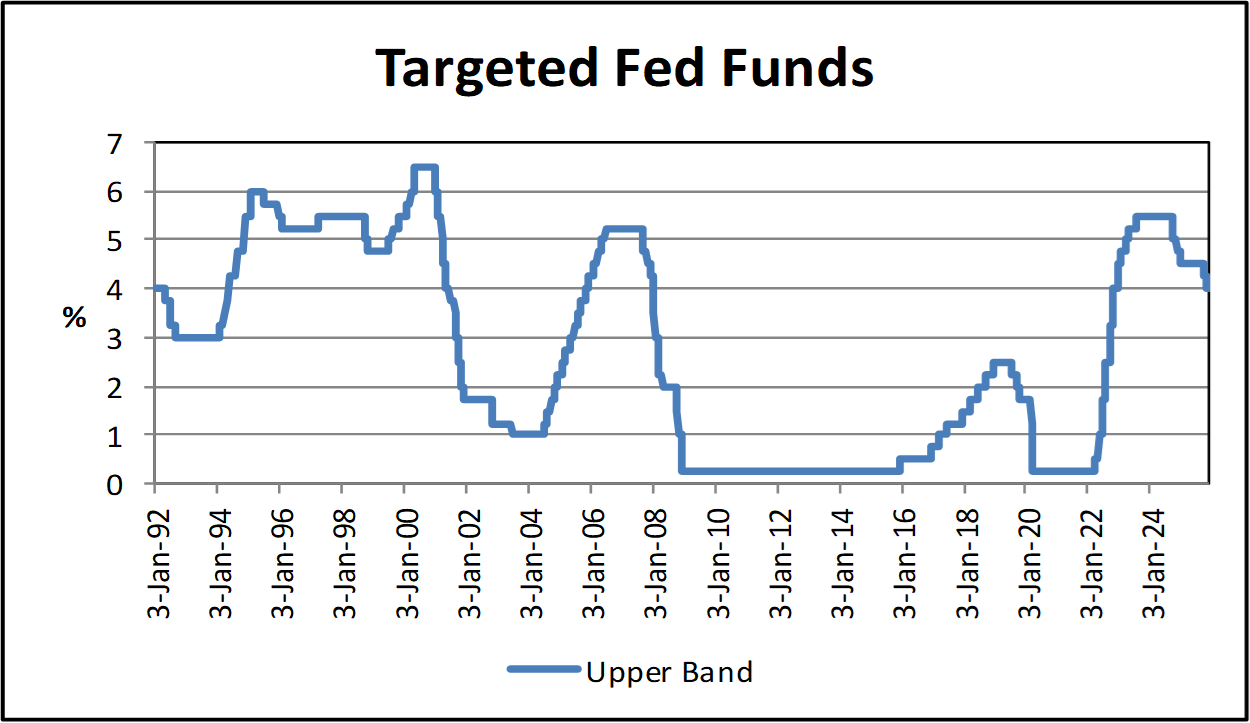

The Fed will announce its next interest rate decision June 17 with the new Fed Chairman Kevin Warsh at the helm. The central bank will likely have little choice but to hold the targeted fed funds range steady at 3.50% to 3.75% for the fourth consecutive meeting due to heightened uncertainty around the economic impacts of the war. The focus of the financial markets will likely center on what can be gleaned about future moves, whether the next move is more likely up than down. Until recently, the financial markets were anticipating two quarter point cuts in the fed funds rate this year, now they are building in the probability of a rate hike.

Kevin Warch comes to the Fed with an ambitious agenda. He has called for “regime change” in policy making, including changing the data the Fed makes its policy decisions on, removing forward guidance from its communications and shrinking the balance sheet. Until recently he was advocating lower rates, and that appeared as a key driver of his nomination by the President. He returns to the Fed as a highly respected economist and former Fed Governor but will need to work methodically if he is to become an effective leader of this group with eighteen other existing members. Only time will tell how long the war will last and what the long-term impact will be. Until more clarity emerges, the Fed will have a hard time moving in either direction. Financial markets will move, however, as they try to predict which side of the dual mandate ultimately gets the Fed back into action, and how effective Kevin Warsh will ultimately be in leading this group.

The minutes of the September 25-26 Federal Open Market Committee (FOMC) meeting reinforced the view of higher interest rate ahead as the economy continues to expand at a solid pace and inflation remains close to its 2 percent target. Economic fundamentals remain strong as evidenced by _____% annualized quarterly growth for the third quarter. While slower than the second quarter’s 4.5 percent growth rate, it is still above trend and of the Fed’s near-term plan to continue gradually lifting short-term rates. Additionally, according to the minutes, a number of participants believe that it will be necessary to raise rates above neutral temporarily to avoid overshooting inflation or contributing to financial imbalances.

Risks to the outlook were seen as roughly balanced. On the downside, trade developments, global divergence of growth prospects and stress in emerging markets were referenced in the minutes, but this was offset by high consumer and business confidence and the potential for a greater than anticipated impact from fiscal stimulus. Despite removing the word accommodative from the last policy statement the majority of FOMC members believe the federal funds rate is still below its neutral level. At 2 to 2.25 percent, the federal funds rates and money market instrument tied to the targeted rates barely or does not cover, depending on which price gauge one chooses, the annual inflation rate, meaning the real cost of money is still cheap, and accommodative.

There is an abundance of data that indicates the economy is on solid footing and will likely continue to expand in the final quarter of 2018 and the start of 2019. The August Job and Labor

Turnover Survey (JOLTS) showed job openings rose to a fresh record high. Industrial production momentum continues at its best pace with output increasing at a 5.2 percent rate, the best in nearly 8 years. The September unemployment rate has dropped to 3.7 percent, a level not seen since 1969. The Conference Board’s leading Economic Index marked its fourth consecutive monthly increase of at least 0.4 percent in September and its 28th straight month without a decline. Taken together, the odds of a recession in the hear-term appear remote.

If there is a canary in the coal mine, it is the housing sector. It is caught in the middle of some powerful headwinds. Recent data has been downbeat as rising mortgage rates and persistently rising home prices are eroding affordability. Existing home sales fell 3.4 percent in September, marking the sixth straight monthly decline. New home sales Housing starts in September declined a sharp 5.3 percent. While some of the weakness in both sales and starts can be chalked up to weather distortions builders still face constraints including available workers, high land prices and rising material prices.

Full Fusion

Full Fusion