April 30, 2026

With the fog of war remaining thick and an incredibly low conviction for how the conflict will evolve, the Federal Reserve needs to be flexible. Facing the stagflationary effects of a supply side shock to the economy, the Federal Open Market Committee (FOMC) elected maximize optionality and in an environment of uncertainty and voted to hold rates steady at their April 28-29 meeting. The Committee believes it is well positioned to deal with the impacts of the conflict that have raised risks to both sides of their dual mandate of price stability and full employment. Supporting the Fed in their policy decisions are underlying financial conditions which show no imminent signs of stress and remain accommodative by historical standards, despite swings in the financial markets. Still, the Fed maintained their easing bias over the objections of several of its members.

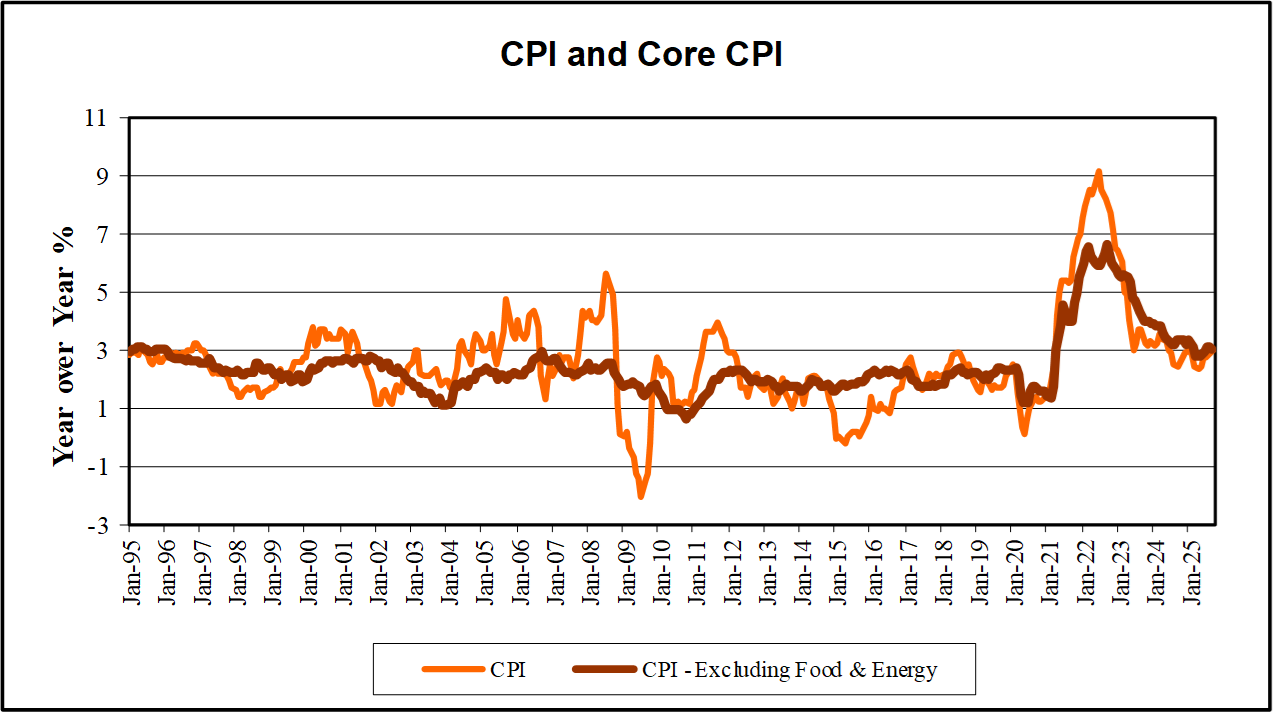

On the inflation front, the Consumer Price Index (CPI) rose higher by 0.9% month-on-month (m/m) in March. On a twelve month basis, CPI jumped to a nearly two-year high of 3.3% from 2.4% in February. The Producer Price Index (PPI) for March also showed a sharp uptick to a three-year high of 4.0% year-over-year. Personal Consumption Expenditures (PCE), the Fed’s preferred measure, was up 3.5% year-over-year. The spillover of higher energy prices into core inflation has been less evident, but will be a key risk the Federal Reserve will be monitoring moving forward.

The April 28-29 Fed meeting was not business as usual. For the first time since October of 1992 there were four dissents. Stephen Miran wanted the fed funds rate cut by 25 basis points. Three others, Beth Hammack, Neel Kashkari and Lorie Logan, supported maintaining the current target range for the fed funds rate, but did not support inclusion of an easing bias in the statement. Despite that easing bias in the statement, the Fed seems unlikely to make any move in the foreseeable future. In the post meeting press conference, we also learned that current Chairman Jay Powell does plan to stay as a Fed Governor for some undefined period past the point Kevin Warsh assumes the Chairman role. While Powell said the Justice Department had assured him they would not restart the criminal investigation into the central bank unless the Fed’s internal watchdog recommended it, he also noted the US Attorney for the District of Columbia has said she might reopen the probe if warranted. Not satisfied as to final resolution, Powell said he will “not leave the board until the investigation is well and truly over with transparency and finality.” So, with Powell staying, it appears Stephen Miran will be leaving to make room on the Board for Kevin Warsh. With the Senate Banking Committee voting earlier in the day to send the nomination of Kevin Warsh to the full Senate, it would appear he will be confirmed and ready to step into the Chairman role on May 15th.

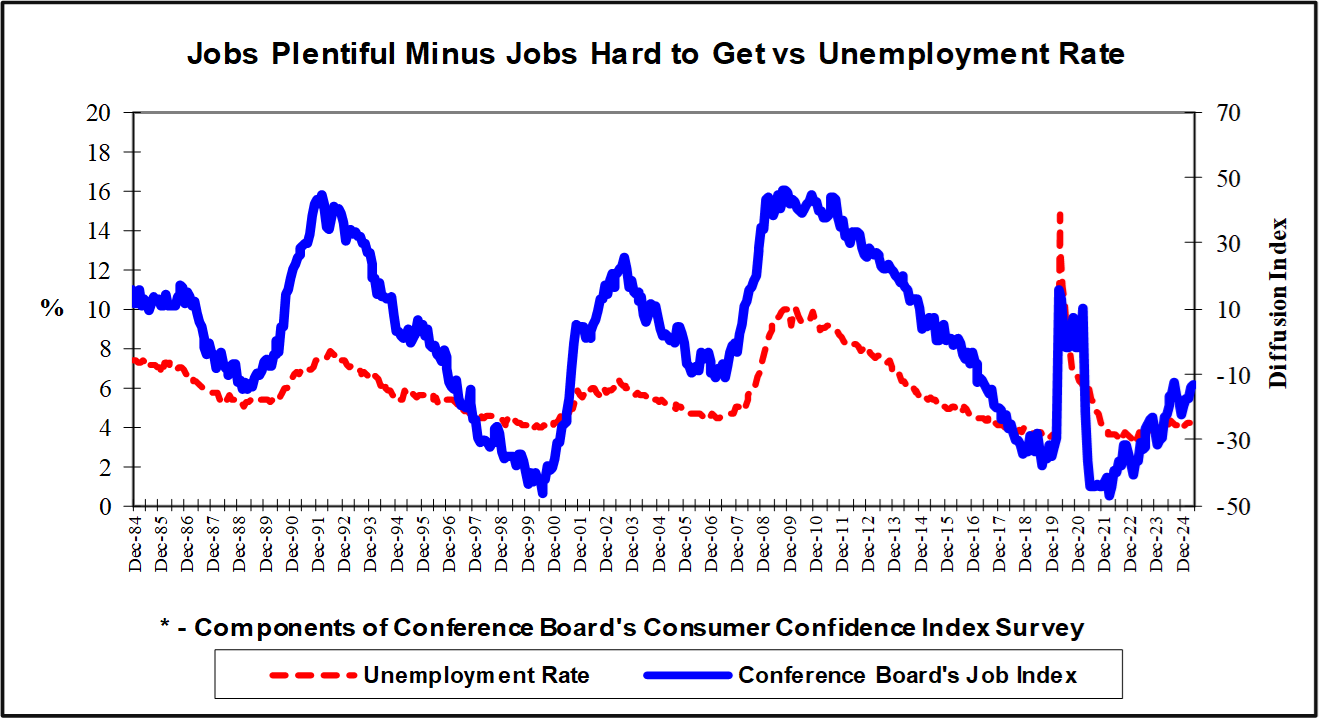

March’s economic data indicated that domestic momentum has not yet broken down. The Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) edged up modestly in March, while the Service PMI registered its 21st consecutive month in expansion territory. Still, these indices have begun to trend downward on rising input costs. Durable goods orders were strong, driven largely by AI related demand. Retail sales surged in March by 1.7%, but it was not just higher spending on gas that drove the increase, as gains were broad based. Ultimately, the outlook for real spending will depend more on the employment landscape and consumers sense of job security. Payrolls surprised to the upside in March, beating expectations. In the employment report’s household survey, the labor force fell by more than civilian employment, pushing the unemployment rate down a tick to 4.3%. Initial jobless claims reported for the April 25 period were a scant $189K, the lowest level recorded since 1969. Looking forward, the Beige Book cited the Middle East conflict was a major source of uncertainty for businesses that complicated decisions around hiring.

The Fed’s dual mandates remain in tension. There are upside risks to inflation and downside risks to the economy and employment. The FOMC currently feels it is well positioned to await further data and is prepared to adjust policy as needed to balance those risks. The likely confirmation of Kevin Warsh as the next Chairman of the Federal Reserve Board in late May or June suggests the Fed may still have path to cutting rates this year, but it should not rule out raising rates if needed.

Full Fusion

Full Fusion