April 30, 2024

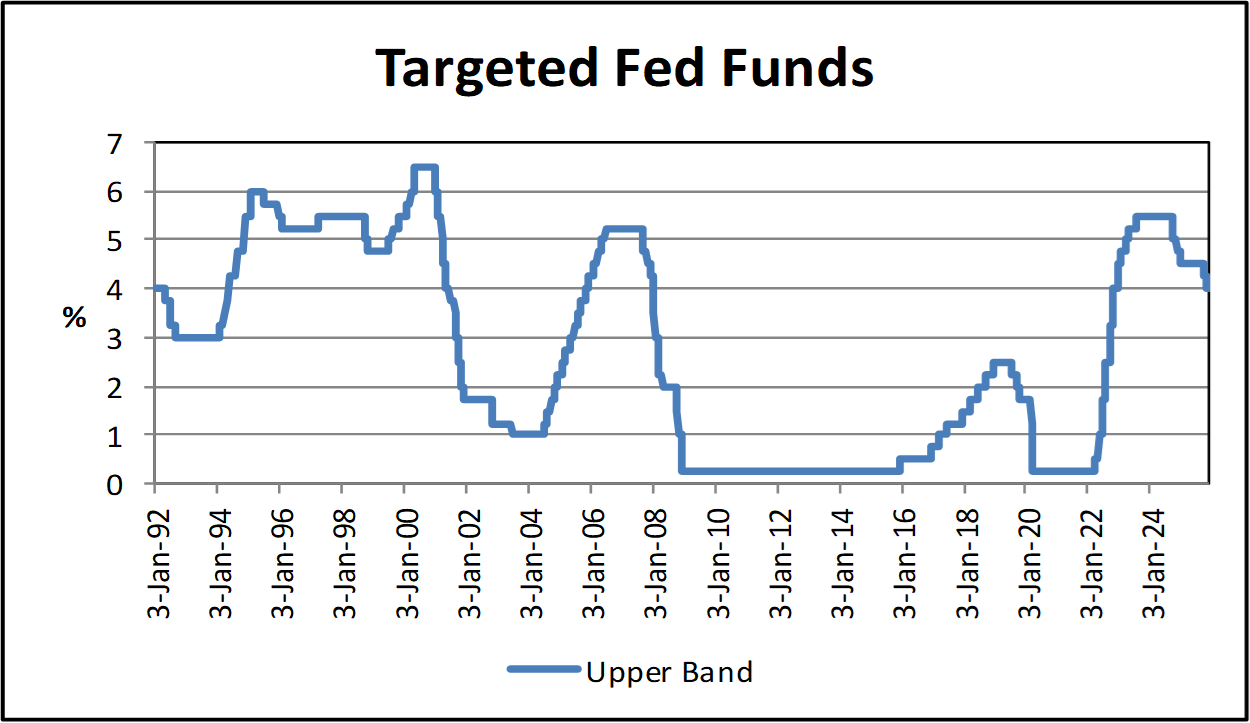

Coming into the April 30 - May 1 Federal Open Market Committee (FOMC) meeting, Fed officials have been consistent in their messaging; policymakers are in no rush to cut rates. Officials are wary of easing too much, too soon, squandering gains in bringing down inflation. They also don’t want to leave rates at levels that unnecessarily slow the economy and cause a severe downturn. The FOMC feels that it can be patient and take time to gain greater clarity about the path of inflation being on a sustainable path lower before easing interest rates. Market participants overwhelmingly expect the FOMC to maintain its targeted range for fed funds at 5.25% to 5.50%.

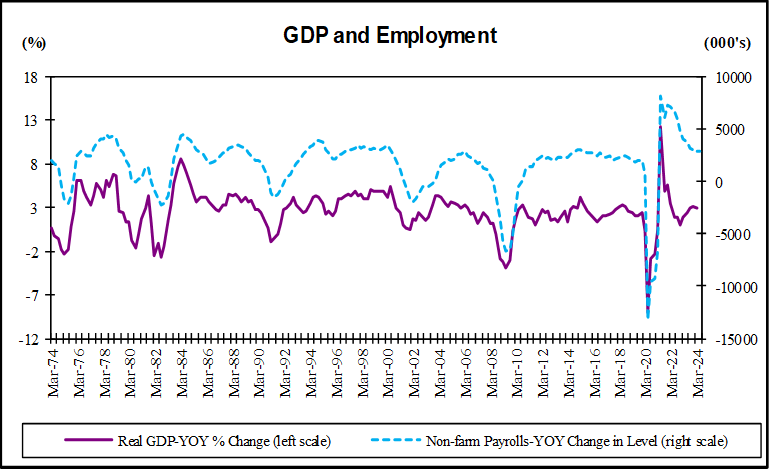

The Summary of Economic Projections (SEP), released at the same time as the policy statement, did have some interesting changes. The Committee’s projections for the economy reflected continued resilience in both activity and price growth. The median projection for real GDP growth in 2024 is 2.1%, up from 1.4% on The December SEP. Growth projections for 2025 and 2026 were also revised up. The Committee’s inflation projections also rose modestly, most notably an increase in the median projection for 2024 core PCE inflation from 2.4% to 2.6%.

Recent inflation gauges have offered less support to the Fed’s mission to re-attain price stability. The headline March Consumer Price Index (CPI) jumped to 3.5% year-over-year, with energy prices seeing positive growth in annual terms for the first time in over a year. Core CPI, excluding food and energy, remained unchanged relative to February at 3.8%. The Personal Consumption Expenditure (PCE) Deflator year-over-year rate ticked up to 2.7%. The core (excluding food and energy) stalled at 2.8%. The data points to ongoing stickiness to inflation.

The labor market remains healthy and has yet to show any meaningful signs of cooling. Job gains have been healthy, posting gains of above 200k in the first three months of the year, with job openings remaining elevated. Because of the strength of the labor market, Fed officials have suggested that inflation data in the coming months will be more critical in determining the timing of rate cuts. Consumers also showed resilience with retail sales in March exceeding expectations and closing out the first quarter on an upswing. While GDP posted a 1.6% annualized quarterly growth rate for the first quarter, down from 3.4% in the fourth quarter of 2023, a wider trade deficit and reduced inventories appeared responsible for much of the decline. Recent economic activity and upside risks to inflation will keep the FOMC in a holding pattern.

In their March meeting minutes, FOMC participants noted they were reluctant to discount the inflation data of the first quarter. They emphasized that they would require greater confidence that it was on a sustainable trajectory to the 2% target before easing policy rates. The data has not been conforming to the Fed’s expectations. The lack of additional progress on inflation and ongoing strength in economic activity means they will need to allow restrictive policy further time to work. Unless some escalation of geo-political events should intercede to force their hand, to ease policy, the Fed needs either more economic slowing or lower inflation.

Full Fusion

Full Fusion